2026 BUDGET FAQ

- Why was there a salary increase in 2026 from 2025 and how much was it?

Total salaries, including payroll burden and benefits, in the 2025 Budget was $884,236.12. Total salaries, including payroll burden and benefits, in the 2026 Budget is $1,108,318.80. This means there has been a total salary, benefits, and payroll burden budget increase of $224,082.68.

This increase in salary reflects the following:

- increases in public works salaries due to collective bargaining agreements and/or annual contractual agreements as well as contractual benefits

- increases in payroll burden imposed by the Provincial and/or Federal governments (i.e. Workplace NL, EI, CPP, etc)

- the additional salary expense for a seasonal equipment operator hired in December which then extended into the 2026 budget year.

2. In 2025 there were no salaries showing under Transportation, Environment Health or Recreation & Cultural Services budgets, but in 2026 there is a total of $326,915.20 shown in those areas, why and where is it coming from?

Previously, salaries for all Town employees were contained within the General Government Salaries and Benefits line items; it was decided after 2024 that specific allocations and records be kept to identify more precisely what the total salary cost is to each service department. During 2025 all staff hours were tracked to determine where each employee spent each hour of their time to facilitate these specifications in the proposed 2026 budget. This data led to the following budgeting reallocations:

Transportation Services: The salaries for transportation services are the only salary alters as a direct consequence of the new seasonal equipment operator. The rest of the amount shown here is the proper allocation of the salary and benefits for the hours worked (based on tracking completed in the 2025 calendar year) by the public works staff on transportation related issues such as road maintenance, snow clearing, etc that was previously contained within the General Government Salaries and Benefits line items. Based on those findings, the 2026 budget for Transportation Services Salaries and Benefits is $135,000.00

Environmental Health Services: There were no additional salaries added to the Environmental Health budget. The salary entered there is the proper allocation of the salary and benefits for the hours worked (based on tracking completed in the 2025 calendar year) by the public works staff on environmental health related issues such as water or sewer that was previously contained within the General Government Salaries and Benefits line items. Based on those findings the amount for the 2026 budget for Environmental Health is $135,000.00

Recreation and Cultural Services: There were no additional salaries added to the Recreation and Cultural Services budget. The salary quoted is the proper allocation of the salary and benefits for the hours worked (based on tracking completed in the 2025 calendar year) by the Community Services Coordinator, and our Summer Camp Workers, which were previously contained within the General Government Salaries and Benefits line items. Based on those findings, the amount in the 2026 budget for Recreation and Cultural Services is $85,915.20.

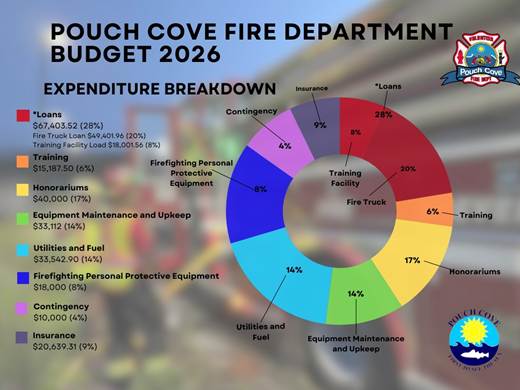

3. Why was there an increase in the Fire Protection budget, and how much was is?

The increase is in the Fire Protection budget is due to:

- Not a true increase, but rather the reallocation of expenses to the appropriate divisions in the 2026 budget. For example; in previous years the cost of insurance and utilities for the PCVFD would have been included in the General Government expenses, whereas these expenses are now included in the PCVFD annual budget allocation specifically.

- The cost of providing services is increasing across all businesses and organizations and despite the best efforts of the Town of Pouch Cove to save money on expenses, inflation will result in additional costs for the same level of service.

This means that while it appears to be a substantial increase from the 2025 budget (and there has been an increase) the difference is more heavily based on reallocation of budgeted funds than true budget increases.

The difference in the Fire Protection budget for 2026 compared to 2025 is $31,695.76. The infographic below (which has been shared on our Town Facebook page) provides a detailed explanation of the expenditures for the Pouch Cove Volunteer Fire Department.

4. Is the new $250 Fire Protection fee to provide salary for the Fire Chief?

No, the $250 fire protection fee is not being used to provide a salary to the Fire Chief, nor is it solely to pay off the pumper truck or other borrowing. This fee represents a shift from a tax-based model (mil rate) to a fee-for-service model to fund fire protection services. All revenue collected through this fee is dedicated exclusively to fire services. These services include; operations, training, equipment, medical calls, and debt servicing related to fire equipment and infrastructure.

5. Under section 3.0 of Transportation Services, what does the term “other transportation services” include, and what is the budget for them?

There is a $10,000 budget included in the 2026 budget to cover cost overruns or unexpected items that may arise in the Transportation Services department. A simple example of these potential costs would be; during a particularly icy winter the Town may need more salt and sand than budgeted. This $10,000 is for those sorts of unforeseen and unavoidable expenses.

6. Why has the budget for water supply increased so drastically for 2026 compared to the 2025 budget?

In previous years water fees would be included under general revenue. With the implementation of the Towns and Local Service Districts Act on January 1, 2025, towns were provided with a three-year period to switch from the existing model to one where all fees imposed for a specific purpose must be spent only on that purpose. Water fees are no different. Instead of waiting three years to implement the new process, the Town of Pouch Cove made a concerted effort to carefully track all spending on any fee related items in 2025 and made a decision to become compliant with the direction two years earlier than mandated. Therefore, under this new model, water fees must be spent only on water and as such there will be a dedicated investment in water related infrastructure spending in 2026.

7. What will this increase in the water budget be focused on in 2026?

After careful tracking of water related fees in 2025, and in compliance with the new processes mentioned above, 2026 water spending will be focused on the Water Treatment Plant, Pumphouse, Screen Chambers and other water infrastructure along with the salaries for public works staff relating to these issues (salaries previously discussed above). This is why there is a larger amount budgeted for Water Supply in 2026.

8. Why is there such an increase in the 2026 Sewage Collection and Disposal budget from that of 2025?

In previous years sewer fees would be included under general revenue. With the implementation of the Towns and Local Service Districts Act on January 1, 2025 towns were provided with a three-year period to switch from the existing model to one where all fees imposed for a specific purpose must be spent only on that purpose. Sewer fees are no different. Instead of waiting three years to implement the new process the Town of Pouch Cove made a concerted effort to carefully track all spending on any fee related items in 2025 and made a decision to become compliant with the direction two years earlier than mandated. Therefore, under this new model sewer fees must be spent only on sewer and as such there will be a dedicated investment in sewer related infrastructure spending in 2026.

9. What will this increase in the sewage budget be focused on in 2026?

After careful tracking of sewage related fees in 2025, and in compliance with the new processes mentioned above, 2026 sewage spending will be focused on the Lift Station and other sewer infrastructure, including an investment of $30,000 in a Wastewater Treatment Plant Fund to allow the Town of Pouch Cove to establish a wastewater treatment plant by 2040 as mandated by the Federal Wastewater Systems Effluent Regulations, along with the salaries for public works staff relating to these issues (salaries previously discussed above). This is why there is a larger amount budgeted for Sewer Supply in 2026.

10. How are the water and sewage rates calculated for 2026?

Water and sewer rates reflect the cost of operating and maintaining the system, including the water treatment plant, infrastructure repairs, regulatory compliance, and ongoing maintenance. While initial estimates were provided when the water treatment plant was commissioned, actual operating costs can change over time due to maintenance requirements, aging infrastructure, and increasing operational expenses. These are all taken into account when calculating the rates.

11. What does “Recreation and Cultural Programs, Activities etc” in Section 6.4 refer to?

While there is no budget for the development of new parks at this time, a portion of the recreation budget is allocated for the upkeep of existing public spaces. This includes basic maintenance, safety measures, and preservation of areas that residents regularly use for walking and recreation. A portion of this budget also relates to regular programs such as summer camp and baby group, as well as events such as Canada Day celebrations and Christmas in the Cove. These are the types of programs that would fall under that section and the 2026 budget has allocated $100,000.00 to support these community endeavours.

12. Pouch Cove doesn’t have a Community Center – what is the Recreation and Community Center budget allocation for?

The 2026 budget quotes $41,695.50 for Recreation and Community Centers; this will be allocated to the Town’s portion of the cost of the Multi-Purpose Court which is anticipated to be completed in the spring of 2026.

13. Will the revenue generated by the new Fire Protection Fee be counted as general revenue?

None of the revenue from the Fire Protection Fee will go into general revenue; all that money will go to the needs of the PCVFD without exception. In previous years, environmental health (water and sewer) fees and PCVFD were combined with tax payments to form general revenue, and the budget for these services were taken from general revenue, but the Town has changed these allocations. In 2026 and going forward, general revenue is used for most expenses outside of environmental health and PCVFD; these service budgets are now being specifically allocated to ensure all funds are spent exclusively in their respective fields.

14. Does every property owner have to pay the new Fire Protection Fee?

No, the fee is not applicable to every property owner in the Town of Pouch Cove. The new Fire Protection Fee is to be applied to property owners who have structures on their land and are therefore requiring further fire protection than those with vacant land. Vacant land owners with no structures on their land will not be required to pay the Fire Protection Fee.

15. Has the mil rate for Pouch Cove changed in the 2026 budget?

The mill rate has remained consistent in the 2026 budget. The cost of providing all mandatory services to the Town has increased, therefore it was decided to implement a Fire Protection Fee to ensure the mil rate would not have had to increase, as well as ensuring that services would not have had to be decreased. With the introduction of a Fire Protection Fee, the existing mil rate is sufficient to cover operational requirements, debt servicing, and the other items included in this year’s budget.

16. Why is the Town spending additional Town revenue instead of reducing taxes?

When inflation rises and costs increase across the economy, a town is forced to spend more money just to maintain the same level of services that the community is used to having.

Here’s how the different factors contribute:

a. Inflationary Costs: General inflation increases the price of:

- Construction materials and equipment

- Road salt and paving supplies

- Office supplies, technology and employee wages

Even if the town doesn’t expand services, it must pay more for the same goods and labor.

b. Tariffs: Tariffs on imported materials (such as steel, aluminum, machinery parts, or infrastructure components) raise prices for:

- Public works projects and vehicle maintenance

- Water and sewer systems

- Municipal buildings

This increases capital project costs and repair expenses.

c. Gas Price Increases: Higher fuel costs directly impact:

- Fire vehicles

- Public works trucks and snowplows

- Parks and recreation maintenance equipment

Fuel is a daily operating necessity, so even small increases significantly affect the annual budget.

d. Electricity Rate Increases: Rising electricity rates affect:

- Street lighting

- Powering municipal and recreational buildings

- Water treatment and pumping facilities

In short, rising inflation, tariffs, fuel, electricity, and cost-of-living expenses increase the town’s operating and capital costs. Without additional revenue, the town would face service reductions, delayed projects, or financial instability.

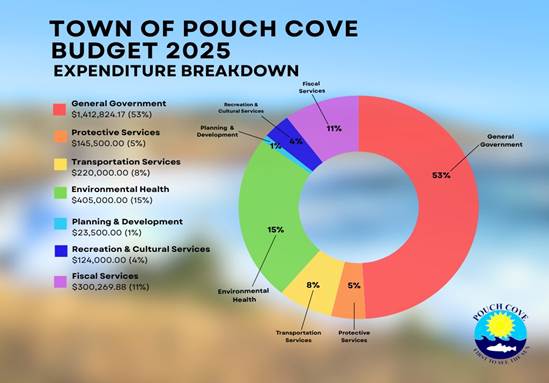

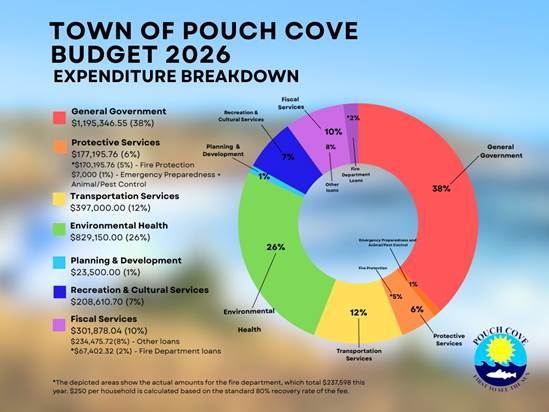

17. Can you highlight the overall changes between the 2025 and 2026 budgets?

As discussed in detail above, there have been increases in the budget due to rising inflation, and municipal regulation changes, as well as a number of budget reallocations to better serve our town moving forward and to remain compliant with municipal mandates coming into effect with the new Towns and Local Service Districts Act of January 1, 2025.

Please see the below diagrams to give a better understanding of the budget breakdowns and reallocations from 2025 to 2026.